By Henry Zupko, MBA, CFP®

As retirement gets closer, it’s normal to feel pulled in a few different directions at once: excited about what’s next, but also uncertain about how to make the numbers work. Add in the complexity of Social Security, and it’s easy to feel behind or confused, especially when it seems like everyone else already has a plan.

And you’re not imagining it; retirement timelines have shifted for many people. Between the Great Resignation of 2021 and 2022 and the post-pandemic changes to how people work, more individuals are leaving the workforce earlier, changing careers, or rethinking their long-term plans. In this environment, understanding how Social Security works and how to claim benefits thoughtfully has never been more important.

This guide was created to help bring clarity to the process and support more confident decision-making, so you can move into the next stage of life feeling prepared, informed, and in control of your Social Security strategy in 2026.

How Are Social Security Benefits Calculated?

The Social Security Administration (SSA) calculates your Social Security benefit. Your benefit is based on your lifetime earnings, specifically your 35 highest-earning years. To qualify, you need at least 10 years of work. If you have fewer than 35 years of earnings, the missing years are counted as zeros. Your historical wages are also indexed to today’s wage levels to account for overall wage growth.

After the SSA determines your average monthly earnings across those top 35 years, it applies a specific formula to produce your Primary Insurance Amount (PIA). Your PIA represents the monthly benefit you’re eligible to receive at your Full Retirement Age (FRA).

That said, the amount you actually receive isn’t always your PIA. Your benefit can be reduced if you start taking Social Security before FRA, or increased if you delay benefits beyond FRA. And beginning at age 62, your eligible benefit is adjusted periodically for cost-of-living increases (COLA).

Spousal Benefits

Married individuals may be able to claim benefits based on a spouse’s work record. A spousal benefit is equal to 50% of the working spouse’s Full Retirement Age (FRA) benefit. To collect a spousal benefit, the working spouse must be at least 62 and must have already filed for Social Security.

The rules change significantly if a spouse passes away. Instead of the 50% cap applied to living spouses, a surviving spouse may be eligible to receive up to 100% of the deceased spouse’s benefit. There are several key distinctions for survivors to keep in mind for 2026:

- You can begin receiving reduced survivor benefits as early as age 60 (or age 50 if you have a disability), which is earlier than the age 62 requirement for standard retirement.

- Survivors can often choose to start one benefit (like the survivor benefit) and switch to another (their own retirement benefit) later. For example, you might claim a survivor benefit at 60 and allow your own benefit to grow until age 70, then switch to your own higher payment.

- If you remarry before age 60, you generally lose eligibility for benefits on your late spouse’s record. However, if you remarry at or after age 60, your eligibility for the survivor benefit remains intact.

Divorced individuals may also qualify for benefits based on an ex-spouse’s work history. To be eligible, the marriage must have lasted at least 10 years, you must have been divorced for at least two years, and you must still be single. You also need to be at least 62 and not entitled to a higher benefit based on your own earnings record. Unlike the rules for currently married couples, your ex-spouse does not need to have filed for benefits in order for you to claim these divorced spousal benefits. If your ex-spouse has passed away, you may be eligible for surviving divorced spouse benefits, which follow the 100% survivor rules rather than the 50% spousal rules.

When Can You Claim Social Security Benefits?

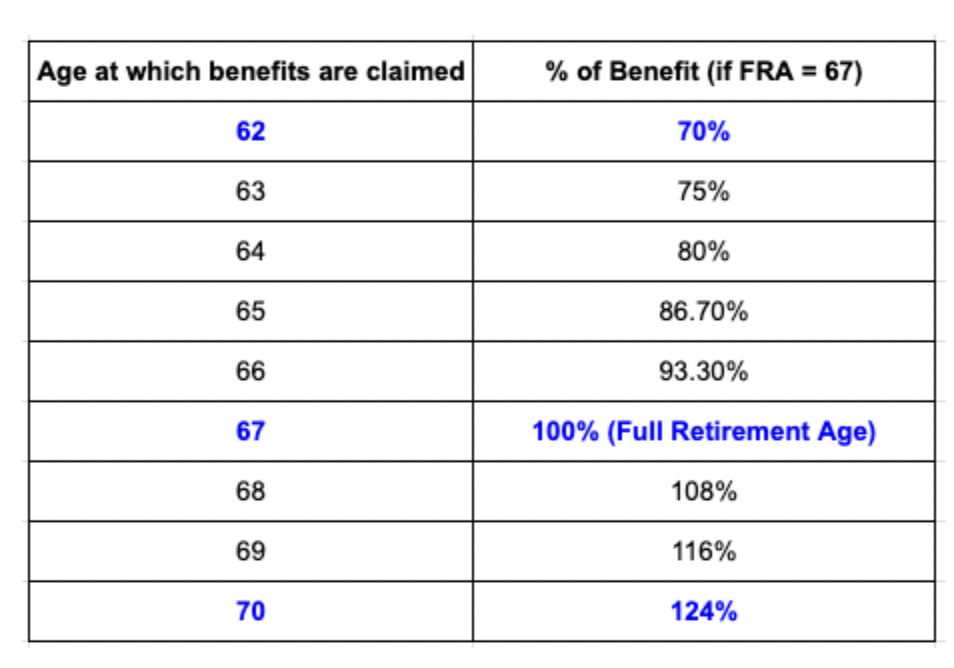

You can start collecting Social Security as early as age 62 or wait as late as age 70. Delaying beyond age 70 won’t increase your benefit any further. But anytime you choose to claim before 70 can affect how much you receive each month.

Early Retirement

You’re allowed to begin Social Security as early as age 62, but doing so typically means a smaller monthly payment than if you waited. Your standard benefit is reduced by a fraction of a percent for every month you claim before reaching full retirement age. Starting early can result in a permanent reduction of up to 30%.

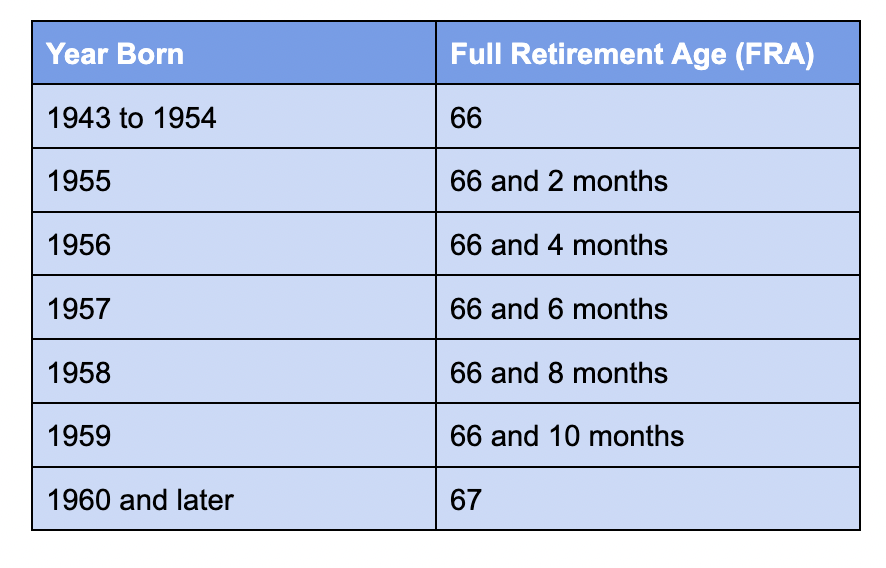

Full Retirement Age

Your full retirement age (FRA) depends on your birth year. For anyone born from 1943 through 1954, FRA is 66. After that, it increases by two months for each later birth year until it reaches 67 for people born in 1960 or later. If you hold off on claiming Social Security until you reach your FRA, you will receive the full primary insurance amount (PIA) you’ve earned.

Delayed Benefits

If you’re still earning income or simply don’t need Social Security right away, you can choose to wait. Delaying can boost your benefit by up to 8% per year, for a total increase of as much as 32%. That increase doesn’t continue forever, however—once you turn 70, there are no additional benefit increases for waiting longer.

When Is the Best Time to Claim Social Security Benefits?

Because your Social Security benefit is calculated using your 35 highest-earning years, staying in the workforce, and especially earning more, can push out lower-earning years and raise your projected benefit. Once you stop working, your benefit is essentially determined by your earnings history, but the age you choose to claim still matters a lot. Starting benefits before full retirement age reduces your monthly payment, while waiting past FRA can increase it by up to 8% per year, up until age 70. Keeping these pieces in mind can help you choose a claiming strategy with more confidence.

Social Security Statement

One key resource to use as you’re weighing your options is your Social Security statement. The Social Security Administration sends paper statements to workers age 60 and older who aren’t currently receiving Social Security benefits and who haven’t created a my Social Security account. Statements are typically mailed about three months before your birthday, but you can also view the same details by setting up an online account through the SSA website.

The statement will tell you your:

- Estimated benefit if taken at age 62

- Estimated benefit if taken at FRA

- Estimated benefit if taken at age 70

- Estimated disability benefit

- Estimated family and survivor benefits

- Medicare information

- Earnings history

Keep in mind that the benefit figures shown are estimates and can change. They’re calculated using your birthdate and projected future taxable earnings.

It’s also important to look closely at the earnings history section and make sure it’s correct. Since your benefit calculation depends on those earnings, errors can impact what you receive. If you spot a mistake, you’ll want to get it corrected as soon as possible.

Deciding When to Claim Benefits

Social Security benefits are determined using detailed actuarial calculations that incorporate life expectancy and assumed rates of return. The system isn’t meant to push people toward retiring earlier or later. If you live about as long as the projections assume, the total benefits you collect over your lifetime should be roughly similar whether you start at 62, 70, or somewhere in between. In other words, you can receive a smaller check for more years, or a larger check for fewer years.

The “right” time to file depends on your health and your personal circumstances. If you anticipate living longer than average, delaying can potentially increase the total you receive over your lifetime because it raises your monthly benefit. On the other hand, if you don’t expect to reach your mid-80s, you may come out ahead overall by claiming earlier even though the monthly amount would be lower.

Once you decide when you want to start receiving benefits, remember to complete your application three months before the month in which you want your retirement benefits to begin.

How Can Married Couples Maximize Benefits?

Since married individuals may be able to choose between their own benefit and a spousal benefit, there are more moving parts to think through when deciding when to file. With a strategic approach, couples can often structure their claiming strategy to increase the total benefit the household receives.

In many situations, one common strategy is for the lower-earning spouse to start benefits earlier, while the higher-earning spouse delays as long as possible. That lets the couple bring in some income sooner using the smaller benefit, while allowing the larger benefit to grow.

Frequently, the husband is the higher earner and the wife is the lower earner, and women tend to outlive men. Using the “delay the larger benefit” approach can increase the higher earner’s retirement benefit while he’s living, and it may also increase the survivor benefit the wife could receive after he passes away.

How Does Working Affect Benefits?

Once you reach FRA, your Social Security benefits aren’t reduced because you’re working—but they can be if you claim before FRA. The earnings rules apply only to earned income, like wages or self-employment income. Income from investments, pensions, or annuities does not reduce your Social Security benefits.

If you are below FRA for the entire year, your benefit is reduced by $1 for every $2 you earn above $24,480. In the year you reach FRA, the reduction is $1 for every $3 you earn above $65,160, but they will only count earnings made in the month before FRA. After you reach FRA, there is no reduction regardless of how much you earn. These thresholds are updated annually, so the amounts may change in future years.

2026 Cost-of-Living Adjustment

The 2026 COLA is 2.8%, slightly higher than 2025’s increase of 2.5%. There is also an increase in the Social Security tax cap. The cap is increased from $176,100 to $184,500, meaning Social Security taxes should not be withheld from income earned above the $184,500 amount.

This increase in benefits may hopefully provide retirees some relief from the rising cost of goods and services. Historically, a COLA that fails to keep pace with inflation only serves to exacerbate financial hardships. It’s important to keep in mind that the COLA might affect pre-retirees and retirees differently. Here is what to expect based on where you are in your retirement journey.

Retirees Taking Social Security

While this increase is good news for retirees, it’s not a license to change spending habits all that much—as most retirees know all too well.

It may still be necessary to keep track of your finances, spending—and, importantly, your tax liabilities; some beneficiaries could experience increased taxes in the coming years, depending on their thresholds.

Retirees Not Taking Social Security

Even if you haven’t started taking Social Security yet, you can still benefit from this increase—there is no requirement to begin benefits this year in order for it to matter. Once a cost-of-living adjustment (COLA) is applied, projected benefits don’t go backward because of it, so those higher payments are intended to remain in place.

On top of that, the removal of the Government Pension Offset (GPO) and the Windfall Elimination Provision (WEP) in 2024 has opened the door to higher benefits for many government workers. In the past, these rules reduced Social Security for people who also received pensions from jobs that weren’t covered by Social Security. With those reductions eliminated, impacted workers may now be able to receive their full Social Security benefits without the prior cut—an important shift for anyone who spent a meaningful portion of their career in government service.

As mentioned earlier, there are also situations where it can make sense to wait a few years after you’re eligible before claiming Social Security. Whether that is beneficial depends on your individual circumstances.

Get Support for Social Security 2026 Planning

Your Social Security decision doesn’t happen in a vacuum. In fact, Social Security claiming choices in 2026 can shape everything from your monthly income to how long your savings may need to last. With multiple timing options and important tradeoffs to consider, it helps to have an experienced Certified Financial Planner® walk you through the details before you file.

At Tranquility Path Investment Advisors, we can assist you in evaluating your choices, understand how Social Security fits into your retirement strategy, and move forward with confidence. If you’re approaching retirement and want a clear plan for incorporating Social Security into your overall picture, we’d love to help. Schedule a no-obligation conversation or reach us at (908) 759-6322.